BoozeBud, the online liquor retailer, has collapsed and entered administration joining a growing list of e-commerce-based delivery services going under.

Established in 2014 by Alex Gale, Mark Woollcott, and Andy Williamson, the company sold a range of beer, wine and spirits products online before being acquired by Carlton United Breweries in 2017.

In 2020, it was sold back to its original founders, Catcha Group and some individual investors.

On Tuesday, the company appointed Michael Brereton and Sean Wengel of William Buck as joint administrators to oversee the sale of the business and its assets. It has stopped taking orders online.

“We have made the difficult decision that the company has insufficient funds to continue operating,” Brereton told News.com.au.

“We have accordingly been forced to stop taking future orders via the online portal… We have also made the difficult decision to lay off staff.”

The administrators aim to secure an investment of funds with expressions of interest sought by May 9.

In December 2021, BoozeBud acquired Get Wines Direct as an independent business which is believed to be unaffected by the decision.

Two weeks ago, BoozeBud’s CMO Dan McMillan, announced on LinkedIn that the brand had completed its site migration to Shopify.

He added the move will enable BoozeBud to become “a leaner, meaner, and more efficient operation with the robust and user-friendly platform.” However, the retailer subsequently abruptly collapsed.

The company’s demise follows the collapse of food-delivery startups Milkrun and Colab last month.

The online pet supplies store Pet Circle has launched an insurance service which offers policies for dogs with coverage of up to $30,000 annually.

Pet Circle co-founder and CEO Mike Frizell (pictured above) said there is a “clear opportunity” as pet parents are “underserved by other pet insurance providers”.

“Our Pet Circle Vet Squad which works in veterinary clinics, told us that many pet insurance policies were not up to scratch, with sub-limits catching out pet parents.

“In fact, about 85 per cent of Australian pet insurance products impose sub-limits that could restrict pets from receiving the best possible treatment.”

The company’s Insurance policies can be personalised with different annual limits for various pets, reimbursements of up to 90 per cent and annual excesses variable from $0 to $150.

To help pets heal from an accident or illness, a 360º Care Optional Extras package can also be added which covers dental illnesses, behavioural problems and supportive therapies like physiotherapy, acupuncture and hydrotherapy.

10 May, 2023

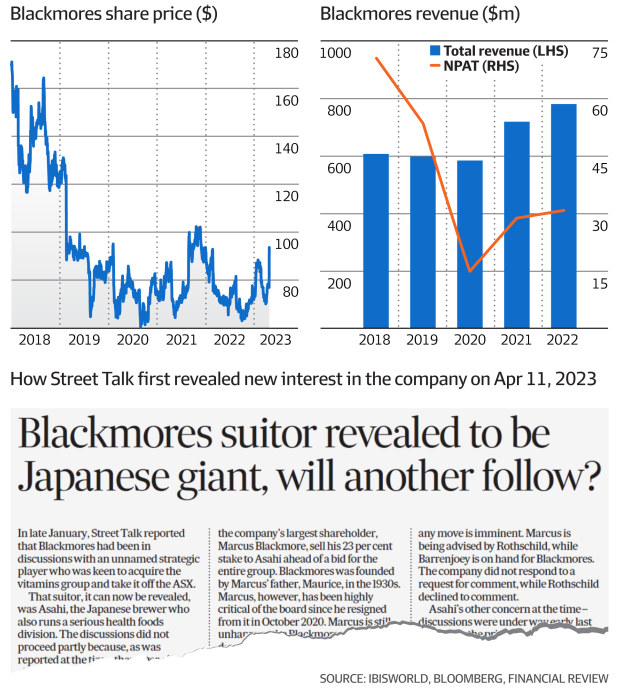

‘Relieved’ Marcus Blackmore to walk away with $334m

Marcus Blackmore, the major shareholder in Australia’s largest vitamins company, Blackmores, will sell his 18 per cent stake into a $1.9 billion takeover by beverages giant Kirin Corporation, which wants to diversify away from a shrinking beer market in Japan.

His strong personal backing, and a separate endorsement from the Blackmores board, is crucial for Kirin, which is offering $95 a share via a scheme of arrangement because it reduces the risk of any rival player emerging.

The acquisition, flagged by The Australian Financial Review’s Street Talk column, is part of a major pivot by the Japanese brewer to reinvent itself as a healthcare and pharmaceutical giant as beer demand shrinks in its home market where the population is ageing.

It also wants to shift its emphasis away from alcohol as part of efforts to be seen a more socially responsible company.

Blackmores shares climbed 22 per cent on the ASX to $93.65 by mid-afternoon on Thursday as the prospect of a second big Australian vitamins company being sold to offshore buyers became highly likely.

Big rival Swisse was bought out by Hong Kong-listed group Health & Happiness in a two-step transaction for $1.7 billion in 2015 and 2016, at a time when Blackmores shares charged through $200 each after a profit bonanza as Chinese consumers sought “clean and green” Australian vitamins brands.

“I’m sort of relieved,” Mr Blackmore said on Thursday.

He is the son of Maurice Blackmore, a pioneer naturopath who established Blackmores in 1932.

Marcus Blackmore took the helm in 1975, two years before his father died, and played a crucial role in building the group to be Australia’s No. 1 vitamins brand.

He stepped down from the board in 2020 and has been involved in a bitter battle with most of the board and management since then, lamenting the progress of the company.

He told The Australian Financial Review on Thursday that he was relieved that a good corporate citizen with a strong culture in Kirin would be the new owner, and that the angst between himself and the board and management of Blackmores over the direction of the company would come to an end.

He said he was also glad it would not be owned by one of the private equity groups that had made regular buyout overtures over the past couple of years. His stake is worth $334 million.

“I got fairly comfortable with them [Kirin]. They’re ethical, they’re strong on culture,” Mr Blackmore said. “Private equity, they would have slashed and gone around sacking people.”

Mr Blackmore, who has just turned 78, has been critical of the board and management of Blackmores over the past few years, and said under the current regime it was unlikely that the company would have delivered the growth it was capable of.

“The company just doesn’t have the resources or the strength. I think Kirin is the best bet,” he said.

New Blackmores chairwoman Wendy Stops said the offer price represented “appropriate long-term value”.

The Blackmores board is recommending that shareholders vote in favour of the scheme in the absence of a higher offer. An independent expert will be appointed to assess the offer and shareholders will vote at a meeting to be held in July.

Over the past few weeks there had been continued speculation about Blackmores being a takeover target for private equity groups, or large Japanese players. Mr Blackmore has received overtures from time to time over the past few years because his stake was crucial to any buyout.

He said his late father had always had a long-term vision of turning Blackmores into the No. 1 vitamins company in the world, and with Kirin’s backing that had more chance of becoming a reality.

The bid documents show his personal stake is 3.52 million shares in the company, worth $334 million at the bid price. There is also a smaller holding in a charity foundation.

Asahi, the Japanese beverages giant that also runs a health science division, made approaches some time ago, but those talks stalled.

Kirin, which owns the Lion beer business in Australia, producing brands including XXXX Gold, Tooheys, West End and Furphy, has been expanding overseas into health drinks and probiotics. It is listed on the Tokyo Stock Exchange and has a market capitalisation of $23 billion.

Kirin announced a three-year business plan last year to invest heavily in research and development and expand in health sciences. Blackmores also offers a strategic advantage because it gives Kirin access to markets in China and South-East Asia where it is not so strong.

“In the health sciences area, Kirin is strong in Japan while Blackmores has a strong presence in Australia, China, and South-East Asia,” senior executive Takeshi Minakata told reporters in Tokyo.

The takeover will need Foreign Investment Review Board clearance.

‘Pretty difficult past couple of years’

The bid comes after an extended period of disquiet last year between Mr Blackmore and the Blackmores board when it was run by previous chairwoman Anne Templeman-Jones.

“It’s been a pretty difficult time for me over the past couple of years,” Mr Blackmore said. During the COVID-19 pandemic, he said, the company had terminated the employment of a lot of its in-house naturopaths who refused to be vaccinated against COVID-19.

“That took a lot of good people out of the business. It was just devastating for me to see that happen.”

Ms Stops, who became chairwoman on November 25, extended the olive branch to Mr Blackmore.

She replaced Ms Templeman-Jones, who had been at the head of the boardroom for two years and with whom Mr Blackmore had what he describes as a “poisonous” relationship.

Ms Stops is also on the board of supermarket giant Coles Group.

Private equity groups seized on the disharmony and early in 2022 there was an approach to try to prise away Mr Blackmore’s shareholding, but that went nowhere because of the upheaval caused by the Russian invasion of Ukraine.

Blackmores was a sharemarket darling in 2016 as booming sales to China pushed profit to a record and lifted its shares to $220. But the ban on tourists to Australia at the beginning of the pandemic in early 2020 and the exit of daigou traders resulted in the stock slumping to about $60 each in early September 2020.

Blackmores chief executive Alastair Symington took the helm in late 2019 at Blackmores after working in Dubai with Coty, owner of brands such as Max Factor and Cover Girl. He had previously worked in executive positions in the consumer goods and health and beauty segment with companies including Nestle, Gillette and Procter & Gamble.

10 May, 2023

World food prices rise for first time in a year, says FAO

The United Nations food agency’s world price index rose in April for the first time in a year, but is still some 20 per cent up on a record high hit in March 2022 following Russia’s invasion of Ukraine.

The Food and Agriculture Organization’s (FAO) price index, which tracks the most globally traded food commodities, averaged 127.2 points last month against 126.5 for March, the agency said on Friday. The March reading was originally given as 126.9.

The Rome-based agency said the April rise reflected higher prices for sugar, meat and rice, which offset declines in the cereals, dairy and vegetable oil price indices.

“As economies recover from significant slowdowns, demand will increase, exerting upward pressure on food prices,” said FAO Chief Economist Maximo Torero.

The sugar price index surged 17.6 per cent from March, hitting its highest level since October 2011. FAO said the rise was linked to concerns of tighter supplies following downward revisions to production forecasts for India and China, along with lower-than-earlier-expected outputs in Thailand and the European Union.

While the meat index rose 1.3 per cent month-on-month, dairy prices dipped 1.7 per cent, vegetable oil prices fell 1.3 per cent and the cereal price index shed 1.7 per cent, with a decline in world prices of all major grains outweighing an increase in rice prices.

“The increase in rice prices is extremely worrisome and it is essential that the Black Sea initiative is renewed to avoid any other spikes in wheat and maize,” said Torero, referring to a deal to allow the export of Ukrainian grain via the Black Sea.

In a separate report on cereals supply and demand, the FAO forecast world wheat production in 2023 of 785 million tonnes, slightly below 2022 levels but nonetheless the second largest outturn on record.

“(The) 2023/24 prospects for rice production along and south of the equator are mixed, largely due to the regionally varied impact of the La Niña event,” FAO said.

FAO raised its forecast for world cereal production in 2022 to 2.785 billion tonnes from a previous 2.777 billion, just 1.0 per cent down from the previous year.

World cereal utilisation in the 2022/23 period was seen at 2.780 billion tonnes, FAO said, down 0.7 per cent from 2021/22. World cereal stocks by the close of the 2022/2023 seasons are expected to ease by 0.2 per cent from their opening levels to 855 million tonnes.

10 May, 2023

Celebrity chef’s meal delivery service Providoor collapses

Fine-dining restaurant meal delivery platform Providoor, founded by celebrity chef Shane Delia at the start of Covid-19, has been forced to close its doors and is likely to be plunged into liquidation.

The shock closure leaves dozens of staff out of a job and high-end restaurants across Melbourne, Sydney and Canberra without the popular home delivery service.

Investors and administrators behind the meal delivery business were working overnight to rescue the company – which was cash flow positive and had only recently raised millions of dollars in new funding – but the decision by one backer to retrieve their investment looks to have sunk Providoor and forced it into immediate liquidation.

It is expected Providoor’s 15 employees will be told this morning that the company was closing, despite the best efforts of founder Mr Delia and other high-profile investors in the company such as the co-founder of employment website Seek, Andrew Bassat, and its chief executive, former eBay boss Tim Mackinnon.

It is also unclear what will happen to the huge number of Providoor vouchers customers are holding and if they can be redeemed.

Providoor had quickly established itself as a high-end restaurant meals delivery service in the weeks following the first pandemic lockdowns in Melbourne in 2020 and soon spread to Sydney and Canberra where it sold meals prepared by well-known premium restaurants for people to enjoy at home.

Top restaurants that used Providoor as their meal delivery service included Mr Delia’s Melbourne eatery Maha where the idea began and other restaurants backed by celebrity chefs including Supernormal, Rockpool, Gwen, Spice Temple, Grossi, Three Blue Ducks, Chiswick, Xopp, The Fold and dozens of other popular establishments.

Providoor was the brainchild of well-known chef Shane Delia who kickstarted the meal delivery business in late-April 2020 in Melbourne as a response to the sudden Covid-19 pandemic restrictions and lockdowns which saw in-house dining banned in restaurants for an extended period.

“It is with a heavy heart that I announce the closure of Providoor, a business borne out of the very worst days the hospitality industry has ever seen,” Mr Delia said.

“While today is a very sad day, I am proud of Providoor and what it has achieved. When people kept using Providoor after social restrictions were lifted, it showed us that it was a really good idea. I just wish it had been given the opportunity to work through the challenging economic conditions, the same facing so many in the restaurant and hospitality sector right now.

“Sadly the Providoor story comes to an end. I want to acknowledge the team, the advisers and our valued restaurant partners who all worked so hard to make Providoor a success.”

Mr Delia, a chef and restaurateur, came up with the idea two days after the cancellation of the 2020 Melbourne Grand Prix after he was forced to send his restaurant staff home due to the restaurant closures.

The owner of well-known Melbourne restaurant Maha had spied a gap in the market where meal delivery services such as UberEats were servicing fast-food and other basic restaurants but that many consumers were looking for a high-end meal experience from their favourite premium eateries.

Since commencing operations, Providoor has made more than 1.2 million meals deliveries and became a major player in Australia’s meal kit sector with 70 restaurants on its platform delivering tens of thousands of meals a week.

Cashflow positive and eyeing off an expansion into Brisbane and the possibly overseas, in November 2021 Providoor went to the market for a selective capital raise seeking between $3m and $15m to fund international expansion plans.

It is believed Providoor had over $5m in the bank when one of the investors exercised a contractual caveat to claim those funds back and despite drawn out negotiations and attempts to save the business this week and which went late into Thursday night it has been tipped into liquidation.

When Mr Delia spoke to The Australian in November 2021 on the appointment of a full-time professional CEO for Providoor, he was upbeat about the huge opportunities for the expansion of the fine-dining meal delivery platform that delivered high quality restaurant meals to people at home.

“We have ambitions to be a global delivery platform and so we need a global player, we want to create a world class team.

“I’m a chef, I’m a restaurateur, I’m a founder of Providoor and my skills set is based on customer experience and relationships.”

10 May, 2023

Vitasoy boss on a mission to reformulate the 25-year-old brand

Vitasoy, one of the earliest brands to introduce soy milk to the Australian market, recently found itself in the centre of a corporate kerfuffle between two global food and beverage giants that created headlines.

The company’s Hong Kong parent company Vita International blindsided Australian dairy giant Bega in October by suddenly announcing it was exercising its right to acquire Bega’s 49 per cent stake in the plant-based milk company, a joint venture between the two struck up in 1999.

However, local chief executive David Tyack is confident not much will change as a result of the new ownership restructure.

But Tyack is hoping to make a splash in other ways. Vitasoy will have to pull off something shy of a brand reinvention if it is to overtake key competitors in the soy milk market – Vitasoy’s “heartland” – against popular rivals Bonsoy, So Good, PureHarvest and Australia’s Own.

And then there is the broader challenge of soy milk’s declining popularity in the face of gathering momentum behind oat milk, which industry leaders (Tyack included) believe will one day overtake soy and almond.

The chief executive, who has led Vitasoy’s Australian operations since September 2019, is under no illusions about the challenges the brand and the business face.

“We were late to the party and we’re trying to play catch-up,” Tyack said of almond milk. Vitasoy introduced an oat milk product 16 years ago and enjoys market leadership in supermarkets but not in cafes. Since Tyack joined the company four years ago, he’s watched the oat milk business expand tenfold in a strong signal that oat, not soy, is key to the future growth of the brand and its stable of products.

Developing brand equity will be Tyack’s biggest challenge. Vitasoy, backed by the $2.7 billion listed parent company, is a well-known brand in Hong Kong, China and other Asian markets, but it has struggled to develop the same currency among Australian consumers despite establishing a local presence 25 years ago.

“We got some work to do to make sure we can still compete with the new, shiny hip people on the block, too,” Tyack said.

“We think there’s value in that master brand for us, even though it includes the word ‘soy’, as being a trusted and known brand.”

The plant-based beverage business has enjoyed high single digit growth over the past few years, according to Tyack, but Vitasoy will have to pick up the pace if it is to hold its own against a competitive landscape and create demand in a declining category.

“We have to be at that level of growth. Otherwise we’re falling away with relevance and [lose] market share.”

The profitability of Vitasoy’s Australian operations is slipping. Its latest annual report lodged to ASIC reveals profits after income tax for the 2022 financial year was $3.7 million, down from $4.2 million in 2021.

Yet, there’s a reason why Vita International paid Bega $51 million to claim full ownership of the company. Despite the market headwinds, Vitasoy Australia punches above its weight within the Vitasoy business itself. Mainland China represents the majority (60 per cent) of Vita International’s turnover, followed by the Hong Kong market at 25 per cent. Australia takes bronze with 8 per cent.

“We’re the most developed Western market for the group,” says Tyack. “We also lead in some other ways.”

Vitasoy Australia has been expanding its plant-based products outside of milk and has found success in its soy yoghurt range, sold in Woolworths, and a range of ready-to-drink bottles of coffee and chocolate with plant-based milk.

The local operation, which has a manufacturing site based in Wodonga, is also a production powerhouse: it exports products back to Hong Kong, Singapore, the Philippines, Taiwan and the Middle East.

But Tyack is devoting most of his energy to making a splash Down Under.

“We recognise that with the influx of global brands, new entrants, you’ve got to keep pace with what the sensory experience is. We’re constantly in internal comparisons with new offerings,” he says.

“Are we at the marketplace with our service, price and quality offer? If we’re not, reformulate.

“We know we’ve got some room to grow in improving our soy offer ... Bonsoy is a very good milk coffee offer ... We’ve got room to improve our almond offer ... There’s still room to improve the oats offer, too.”

Australia’s biggest private convenience store operation, 7-Eleven, is up for sale and could deliver the two families who own the franchise chain a multibillion-dollar payday.

“The Withers and Barlow families have decided that the time is right to review options for the future ownership of the business with a view to setting it up for future growth and success,” Russell Withers said on behalf of the 7-Eleven shareholders.

The chain was started by the billionaire businessman Withers and his late sister, Beverley Barlow, in the 1970s. It had grown from a single store in suburban Melbourne in 1977 to become one of Australia’s largest fuel and convenience retailer, with a network of about 750 stores across Victoria, NSW, ACT, Queensland and Western Australia, Barlow said.

The sales process comes one year after the group paid about $100 million in a class action settlement with franchisees after an investigation by this publication and the ABC’s Four Corners program uncovered evidence that the convenience store chain was engaged in systemic wage theft and doctoring of payroll records.

The chain was also forced to pay back more than $173 million to workers, although former Australian Competition and Consumer Commission boss Allan Fels, who previously headed the repayment panel, said that it did not reflect all the unpaid wages.

After the settlement last year, chief executive Angus McKay said 7-Eleven was pleased the matter had come to an “acceptable resolution”, and added the company had also invested $50 million in systems to prevent wage theft, and training for franchisees.

7-Eleven Holdings chairman Michael Smith said in a statement on Monday that the sales process was at an early stage and was expected to take months.

“7-Eleven has an unrivalled brand and convenience footprint in the attractive fuel and convenience market in Australia,” he said.“The business has great momentum and a compelling strategy for growth across convenient food, the continued transformation of our total merchandise offer, digital and format innovation, and new stores. With such a strong platform in place, the shareholders have decided that the time is right for new ownership of the business to oversee the next phase of our growth and development.”

The company was not providing any further details of the sales process, which has commenced, but a listing on the ASX is considered unlikely given the state of the sharemarket, meaning a trade buyer is the most likely option.

While no one is currently offering a valuation of the privately owned business, a sale could yield billions for the owners, based on recent transactions.

Last month, ASX-listed Viva Energy acquired South Australian fuel and convenience store business OTR Group for $1.15 billion. OTR has 174 integrated fuel and convenience stores in South Australia.

7-Eleven is the third-biggest convenience store operator in Australia behind Viva and Ampol, according to RBC Capital. It owns 250 stores, with the remaining 500 consisting of franchise operations. Integrated fuel and convenience stores account for 612 of its outlets with 192 directly owned by 7-Eleven.

A slow start to seasonal winter sales is affecting growth in Big W’s apparel category in the third quarter of FY23, despite overall sales growth of 5.7%.

The discount department store reported total sales in Q3 increased to over $1 billion, with a 4-year compound annual growth rate (CAGR) of 7.2%.

Homewares, leisure and toy sales recorded the strongest gains, offset by more subdued growth in apparel.

While eCommerce sales declined 1.9% to $91 million, store sales grew 6.5% to $955 million in the quarter.

This was driven by an increase in comparable transactions of 6.8% as customers returned to shopping in store more frequently. However, this was somewhat offset by a decline in items per basket.

Sales growth moderated through the quarter after cycling the COVID-driven impact in the prior year.

Woolworths Group CEO Brad Banducci said inflation in many areas remains "frustratingly elevated" with plans to provide customers with greater value in their shopping baskets.

This includes leveraging own and exclusive brands, its Price Dropped program and personalised Everyday Rewards member offers across its portfolio.

“Our current focus is on continuing to improve our customer experience, especially value for money and product availability, and we remain cautiously optimistic that Woolworths Group is well-placed to navigate and respond to the current trading challenges successfully for all key stakeholders – our customers, our team, our suppliers and community partners, and our shareholders.”

Big W has already leveraged sales across MyDeal, which was acquired by Woolworths last year.

10 May, 2023

Coles sales increase in third quarter, opens new automatic DC

Coles says sales volumes improved in the third quarter despite mounting cost-of-living concerns and inflation.

For the 12 weeks to March 26, group sales increased 6.5 per cent to $9.7 billion as consumer hospitality spending and increased immigration drove growth.

Supermarket sales grew 7 per cent to $8.6 billion supported by an expansion of the ‘Dropped & Locked’ value campaign and the commencement of the MasterChef Cookware continuity program.

E-commerce sales increased 2.7 per cent to $662 million partially driven by Click & Collect Rapid sales, contributing 7.5 per cent to all supermarket sales.

The business’ liquor division registered sales of $801 million, up 2.6 per cent driven by e-commerce sales growth of 28.9 per cent (or by $43 million) as well as growth in the retailer’s Exclusive Liquor Brands (ELB) division of 15.2 per cent.

Liquorland was the strongest-performing banner with ready-to-drink a key performing category.

C-store sales from discontinued operations reached $271 million, up by a marginal 0.7 per cent. The Coles Express Fuel business sale to Viva Energy is expected to be completed by the end of May.

“We remain confident that we are well positioned to navigate the current macro environment and deliver trusted value for our customers at a time when many households are experiencing increasing financial pressure,” said the retailer in a statement

The company also opened its first automatic distribution centre in Redbank, Queensland yesterday.

27 Apr, 2023

‘Why would I?’: Founder Irene Falcone won’t buy Nourished Life back from BWX

Entrepreneur Irene Falcone has ruled out buying beauty e-commerce platform Nourished Life, which she founded in 2011, back from collapsed cosmetics empire BWX, which has listed Nourished Life and another online retailer for sale.

Falcone founded Nourished Life as a blog before it became an online marketplace dedicated to natural and clean beauty products, and sold it to BWX in 2017 for $20 million.

However, the troubled parent company is now seeking buyers for Nourished Life and eco-friendly marketplace Flora & Fauna in a move that will swiftly shrink its stable of brands, while it also scrambles to offload its stake in celebrity cosmetic lines Go-To Skincare and Purely Byron.

But Falcone said BWX had done such a poor job of operating Nourished Life that she would not consider repurchasing the platform, a move that would have echoed make-up mogul Zoe Foster Blake’s pole position to buy Go-To Skincare back at a bargain-basement price.

“When you shopped at Nourished Life, you knew every single ingredient was clean, checked, had complied with this amazing matrix of ingredients policies. Since I left, I’ve seen ... a whole bunch of rubbish there,” she said. “Why would I pay money for it?”

“I wouldn’t want to buy it back for that reason. It’s just tarnished now.”

KPMG’s David Hardy, Gayle Dickerson, James Stewart and James Dampney have been appointed as receivers and managers handling the day-to-day operations of Nourished Life and Flora & Fauna, together known as BWX Digital. They are now eliciting “urgent expressions of interest to acquire or recapitalise” the platforms’ assets and operations.

“BWX Digital comprises Nourished Life and Flora & Fauna, two of Australia’s leading e-commerce platforms operating multi-category portfolios of eco-friendly, natural and organic, toxin-free, health, wellbeing and lifestyle products,” KPMG said in a statement.

The sale of the e-commerce platforms marks the third and fourth business that BWX, itself in voluntary administration, is offloading following the high-profile and likely return of Go-To to Zoe Foster Blake, and the collapse of Elsa Pataky-founded cosmetics line Purely Byron in March. BWX owns 47 per cent of Purely Byron, which has appointed administrators to find a new owner.

BWX’s remaining brands are Sukin, Andalou and Mineral Fusion, the first two of which are sold through pharmacy and supermarket retailers Priceline, Woolworths and Coles.

“BWX Digital is also in voluntary administration, meaning interested parties can consider a sale as a going concern, a recapitalisation or restructuring of the business through a Deed of Company Arrangement [DOCA],” KPMG’s statement said.

Spanning skincare, make-up, eco-friendly home and baby products, food, health and pet merchandise, Nourished Life and Flora & Fauna sell a combined 590 brands and nearly 13,000 products, and together made net sales of $32.5 million in the 2022 financial year. The brands have a combined 115,000 customers considered “active” and 337,000 loyalty program members.

The hasty sales process will last for barely 48 hours, with expressions of interest closing at 5pm on Friday.

The two sites appear to have ceased trading – customers have been barred from making purchases and the checkout process has been blocked.

“We’re sorry but our checkout page is currently unavailable. We are working to get it back up and running as quickly as possible,” says a banner on Nourished Life’s website. “If you need anything else from us, please contact our lovely customer care team.”

The Flora & Fauna website permits users to add items to their shopping cart, but posts a similar message when attempting to check out.

“Checkout currently unavailable,” users are told. “In the meantime, please feel free to continue browsing our website and adding items to your cart or wishlist. Rest assured that your items will be waiting for you when our checkout page is back online.

“Keep an eye on the main page for updates. We appreciate your patience and understanding during this time, and we hope you have a lovely day!”

Some social media users have posted comments under Nourished Life’s latest Instagram post querying when the checkout process will recommence.

While KPMG have been appointed manager and receivers of the two platforms, representing secured creditors, FTI Consulting have been appointed by the BWX board as administrators.